Cashflow & Debt Reduction

Overview

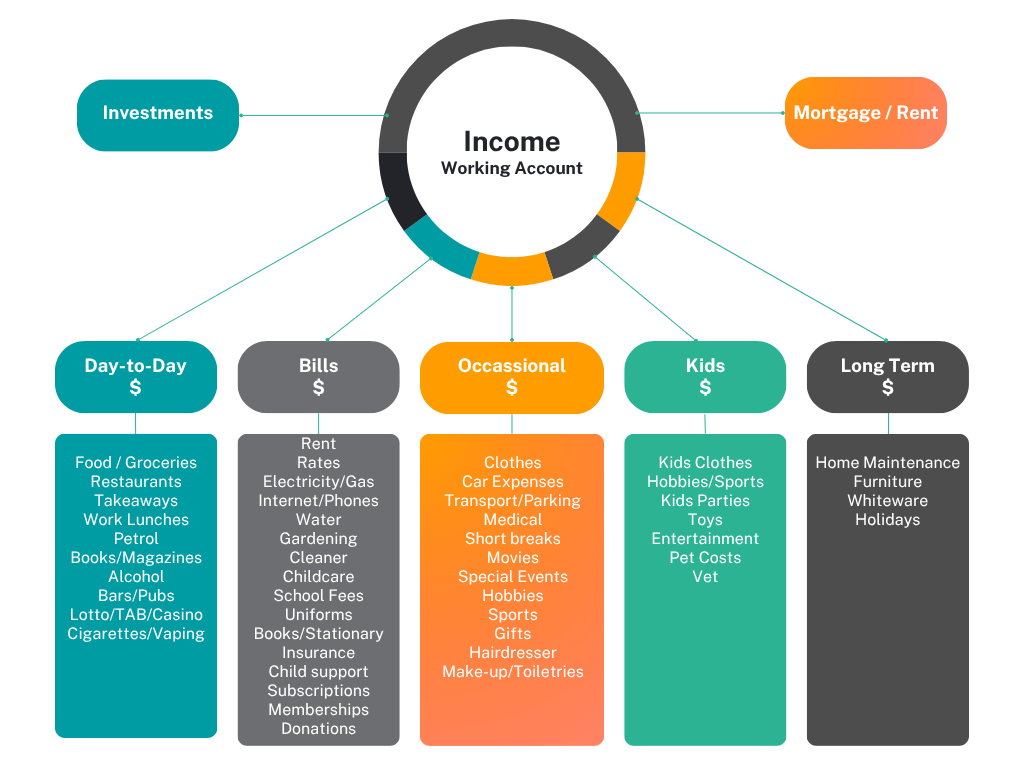

Cashflow management is the foundation to financial success.

Here is one way to easily manage your money - without spreadsheets, tracking or coding.

It’s your own personal filing system.

If everything gets dumped into one bucket, it’s easy for things to get messy.

Cashflow Management

To successfully follow the accelerated mortgage elimination plan,

there’s one key element that can’t be overlooked:

staying on track with your personal spending.

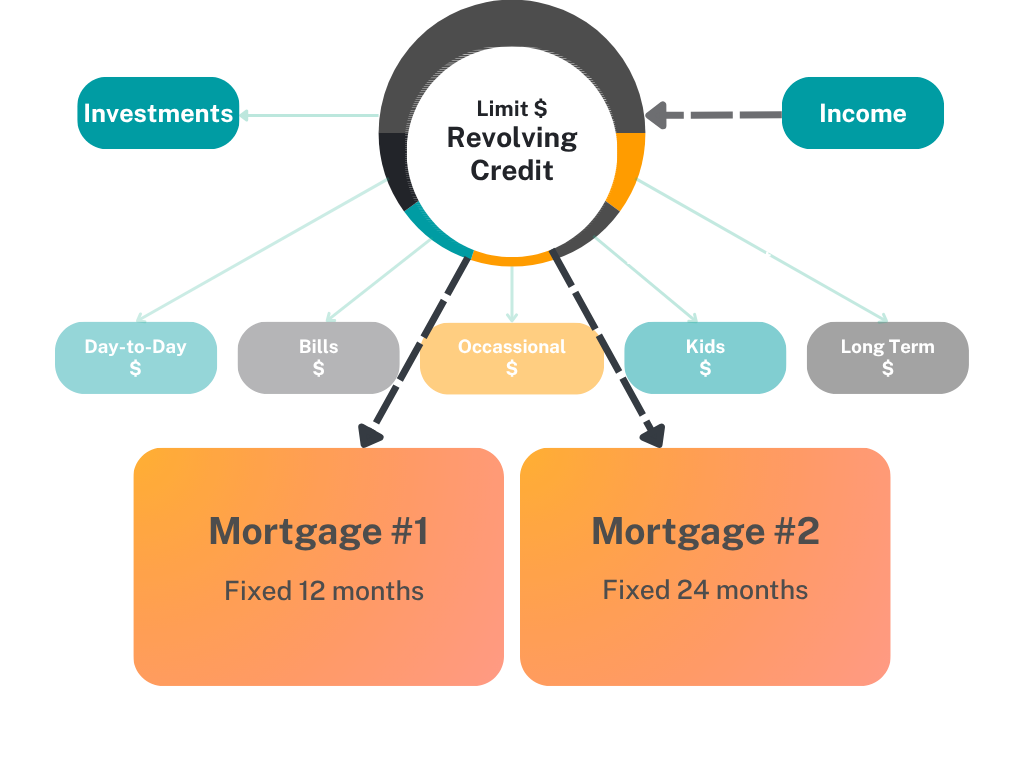

Mortgage Management

It’s clear that putting more money into your mortgage will save you interest and help you pay it off years sooner.

Most people understand that in theory. The reason it often doesn’t happen in practice is because the right structure isn’t in place.

Without the right structure, it quickly becomes hard to manage and the plan slips away.

In this strategy, the mortgage is split into three parts:

•A revolving credit / offset / personal transaction facility

•One fixed loan for 12 months

•One fixed loan for 24 months

This approach reduces interest rate risk by staggering the fixed terms. Instead of having your whole mortgage exposed to rate changes at once, we spread it out. Each year, about half of your mortgage will be up for review, and each time we’ll refix that portion for 24 months.

This creates a more stable, balanced average interest rate over time.

How it Works in Practice

•At the end of the year, when Loan 1 comes up for review, we use the surplus you’ve saved in the revolving credit to make a lump-sum repayment.

•We then refix that loan for another 24 months.

•The revolving credit balance resets, and the cycle begins again.

This structure is achievable as long as you stick to the budget you’ve set. What I like most about it is that it gives you very specific, short-term goals to focus on every 12 months (we can even make it 6 months if you’d prefer), making the long-term mortgage repayment journey much more manageable.

Key Benefits

•Reduces the loan term down to years, giving you more time to save for retirement.

•You will save in interest costs alone.

•Lower interest rate costs by keeping the majority of your loans as fixed mortgages.

•Less interest rate risk by staggering fixed terms.

•Revolving credit facility provides flexibility, access to funds and ability to pay down debt faster on your terms.

Things That Get in the Way

In my experience, the biggest distraction for clients is interest rates. Of course, we always want to secure a sharp rate - but the reality is that most banks are very similar, and their advertised offers can almost always be negotiated.

What makes the real difference over the long term isn’t the rate, it’s the structure. The right structure sets you up for success, keeps things manageable, and helps you stay on track to actually achieve the plan.

Staying on Track

To help you stay on track, the table below shows your target (accelerated) mortgage balance for each month over the next 12 months. This gives you a clear, short-term goal to focus on. Seeing your progress month by month can be motivating, and incredibly rewarding to watch your balance come down.